INVESTMENTS • READ TIME: 5 MIN

"It is a tenet of my investment style that, on the subject of common stock investment, maximizing the upside means first and foremost

minimizing the downside. The deleterious effect of permanent capital loss on portfolio returns cannot be overstated."

Michael Burry

Insofar as taxes are a certainty in life, so too are drawdowns for investors. While neither of these are particularly pleasant, they are fundamental aspects of investing, earning a wage, taking distributions from an account, etc. The aim is not to dwell on the unpleasant "unavoidables,” but to instead consider the ways in which their effects on portfolio returns can be muted - or, in some cases, eliminated.

As is the case with nearly any investment strategy, patience, discipline, and time (a long-term perspective), help combat losses and “return detractors.” However, it is just as important to attempt to mitigate losses and tax drag due to the benefit of compounding returns - as in, with less lost (conversely, with more gained) the effects of compounding can provide greater potential returns.

In the Midst of a Drawdown

It’s unrealistic to hope (or assume) investments will only increase in value - take a look at the first half of 2022 if there’s any doubt to that statement. There are a few ways to approach portfolio losses - realize losses and convert to cash, stay invested, or contribute additional funds (if possible) to the account. Options one and two are reactionary choices and would most likely only be considered if declining values felt significant - meaning, a 1-20% drop may be unpleasant, but is hardly outside of the norm. Option three, contributing additional capital, is most likely part of an ongoing, systematic purchase plan or an attempt at buying when markets are low.

However, by the time an investor feels compelled to action after/during a downturn, assuming no dramatic shifts in fundamentals, market conditions or outlooks, etc. have occurred, it’s likely the least opportune time to make any adjustments (barring contributions of additional capital since the lower securities prices fall, the greater their expected return...)

How, then, can drawdowns and risk be mitigated? Additionally, to what extent does this element of forethought have on overall returns? Quite a bit, actually.

As outlined previously - What We're Talking About When We Talk About Risk - one of the most crucial elements of portfolio management and financial planning is risk management. In particular, risk management encompasses tailoring volatility to an acceptable level while also attempting to limit the severity of drawdowns when they occur.

The Arithmetic of Loss

While an appropriate, diversified allocation to equity, fixed-income, etc. varies by investor, the mathematics of loss (drawdowns) are uniform. A 5% gain in “Portfolio A” is the same as a 5% gain in “Portfolio B.” Conversely, a 10% loss sustained in each portfolio, mathematically, means the same thing.

Understanding, conceptually, the mathematics of loss highlights the significance of risk management. A portfolio (or single investment) loss requires a return greater than said loss to “get back to even” - this can be expressed in the following way:

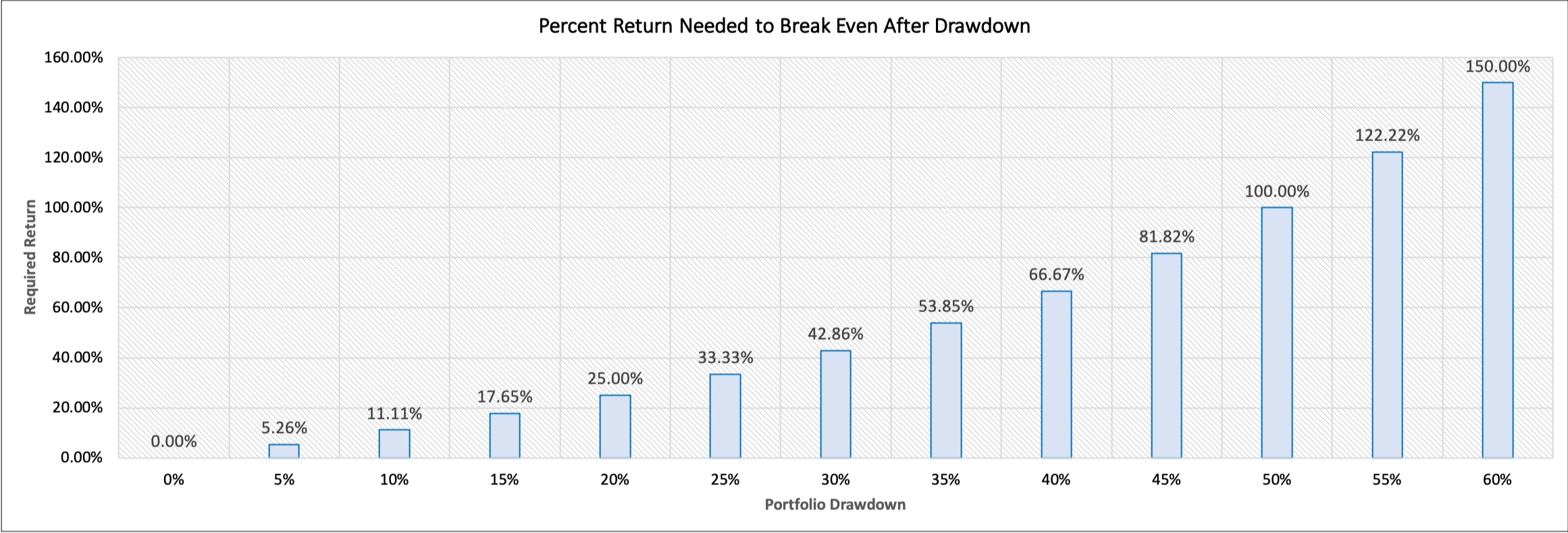

[ 1 / ( 1 - Loss Percentage ) ] - 1 = Gain Required for Breakeven

For example, assume a portfolio loss of 20% - therefore, [1/(1 - .2)] - 1 = .25 or 25%. The following graph illustrates how “deeper” losses require increasingly significant (which, almost certainly, requires greater time) returns.

Given the information/illustration above, reducing losses - “muting the severity of drawdowns” - is more impactful to a portfolio than maximizing gain. In short, the arithmetic of loss shows that a loss impacts a portfolio more than a comparable gain benefits it. Apart from the pure mathematics of loss, there is also evidence to suggest that the psychological toll of loss far exceeds the pleasure of gain - see 5 (Mis)Behaviors Affecting Your Financial Wellness.

These factors all illustrate the importance of (1) appropriately defining and controlling risk, (2) incorporating relevant strategies to limit portfolio losses including (but not limited to) diversification across asset classes and tactical management, and (3) maintaining flexibility in distribution schedules and/or sources of distributions.

How Taxes Impact Portfolio Returns

Another detractor to account for in the construction and management of an investment portfolio is tax (federal and [for most] state.) While appropriate asset allocation attempts to reduce portfolio drawdowns, asset location seeks to limit the tax drag on portfolio returns.

What is Tax Drag?

Tax drag refers to the reduction of potential income/returns due to taxes. Tax drag is particularly relevant for non-qualified (taxable) accounts as both intra-account transactions (buying, selling, rebalancing) and withdrawals generate taxable events. In the case of most qualified accounts (IRAs, 401(k)s, etc.) taxation occurs at the time of distribution.

To what extent, then, does asset location aid in decreasing tax drag on a portfolio? By selecting the appropriate account(s) to place investments, the taxable capital gains, interest payments, etc. may be reduced or eliminated - for example, place the most tax inefficient assets (corporate bonds paying a regular coupon) in the most tax efficient vehicle (an Individual Retirement Account). By reducing or eliminating taxable events, be it through qualified accounts or tax-preferenced investments (such as municipal bonds), the portfolio is shielded from many elements of tax drag.

To illustrate this point, consider the following example: if a municipal bond is yielding 5% per year in interest payments, what would an equivalent yield be for a taxable bond? Assuming the investor’s marginal tax rate is 30%, a 5% municipal bond (tax-free) is equivalent to a taxable bond yielding 7.14%. Expressed as a formula, the calculation is:

Tax-Free Bond Yield / (1 - Marginal Tax Rate)

The scenario above illustrates the significance of both selecting appropriate investments and placing these investments in the appropriate types of accounts to maximize possible returns. As is prudent in any situation, proper consideration to tax brackets, availability of accounts, etc. is essential in the overall creation and implementation of an investor's financial plan.

Other Relevant Detractors (& Contributors)

In addition to proper asset allocation, asset location, etc. there are a number of other strategies available to investors to attempt to “keep” more of what has been made, as well as limit the impact of return detractors. Tax-loss harvesting, systematic rebalancing, diversification across assets and asset classes, utilization of tax-advantaged accounts, etc. all provide additional means of generating portfolio alpha.

To summarize, one of the most effective ways to generate alpha - as in, produce returns over and above the market - is to be aware of and preempt the impact of portfolio detractors. While the short-term impacts of tax-loss harvesting, informed asset placement, etc. are not immediately impactful, those "savings" allow for additional funds to compound in a portfolio over time.

The content is developed from sources believed to be providing accurate information. All investing involves risk, including the possible loss of principal, and there is no guarantee that any investment strategy referenced here will be successful. The information in this material is not intended as tax or legal advice. It may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. This material was developed and produced by RP Wealth Advisors to provide information on a topic that may be of interest. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security. Diversification and asset allocation are methods used to help manage investment risk; they do not guarantee a profit or protect against investment loss.